An iron condor can look responsible on paper.

Four option legs. A maximum loss. A maximum gain. A neat payoff diagram with a flat profit zone in the middle and two cliffs on the sides.

The trader is not supposed to be naked. The wings are bought. The risk is capped. The trade has a name that sounds more like portfolio construction than gambling.

Then the trade is repeated.

Then the size changes.

That is where the Captain Condor file stops being a story about one options structure and becomes a story about account risk.

MarketWatch reported in early January that options trader David Chau, known online as "Captain Condor," and followers of his trading approach suffered a wipeout of more than $50 million around the end of 2025. Interactive Brokers later republished a Barron's column that cited the same MarketWatch reporting and framed the episode as a warning about self-described options experts.

The exact private trade records are not public. The public story is still enough for a risk file: a strategy presented as controlled risk can become uncontrolled at the account level when exposure keeps growing.

The point is not that an iron condor can lose.

The point is that the loss became too large to be just another loss.

What The Trade Promised

An iron condor is a range trade.

The trader sells an out-of-the-money call spread and an out-of-the-money put spread on the same underlying, often an index such as the S&P 500. If the index stays between the short strikes until expiration, the trader keeps the premium. If the index moves too far in either direction, one side of the structure can approach maximum loss.

The attraction is clear. The trader can say, before entry, what the maximum loss is for one spread. That makes the trade feel cleaner than shorting naked options.

But "defined risk" is not the same thing as "small risk."

Defined risk means the loss on a specific structure has a boundary. It does not mean the trader chose a size the account can survive. It does not mean the trader will stop after one bad cycle. It does not mean the market cannot move through the range faster than the trader expected.

One spread can be defined.

The campaign can still be too large.

The Range Trade Has A Bad Habit

Short-premium trades can feel best right before they hurt.

Most days, the market does not make an extreme move. Time passes. Premium decays. The trader gets paid for waiting. The account sees a stream of smaller wins, and the strategy begins to feel less risky than it is.

Then the range breaks.

That moment is not rare in a philosophical sense. It is only rare compared with the number of calm days before it. The calm days are what make the trade seductive. They also train the trader to expect the next move to stay inside the lines.

Captain Condor was not the first options trader to discover this. He was just a very public version of an old problem.

The dangerous trade is not always the one with unlimited theoretical loss. Sometimes it is the one with a maximum loss printed clearly on the ticket, multiplied by enough contracts to make the boundary too large to absorb.

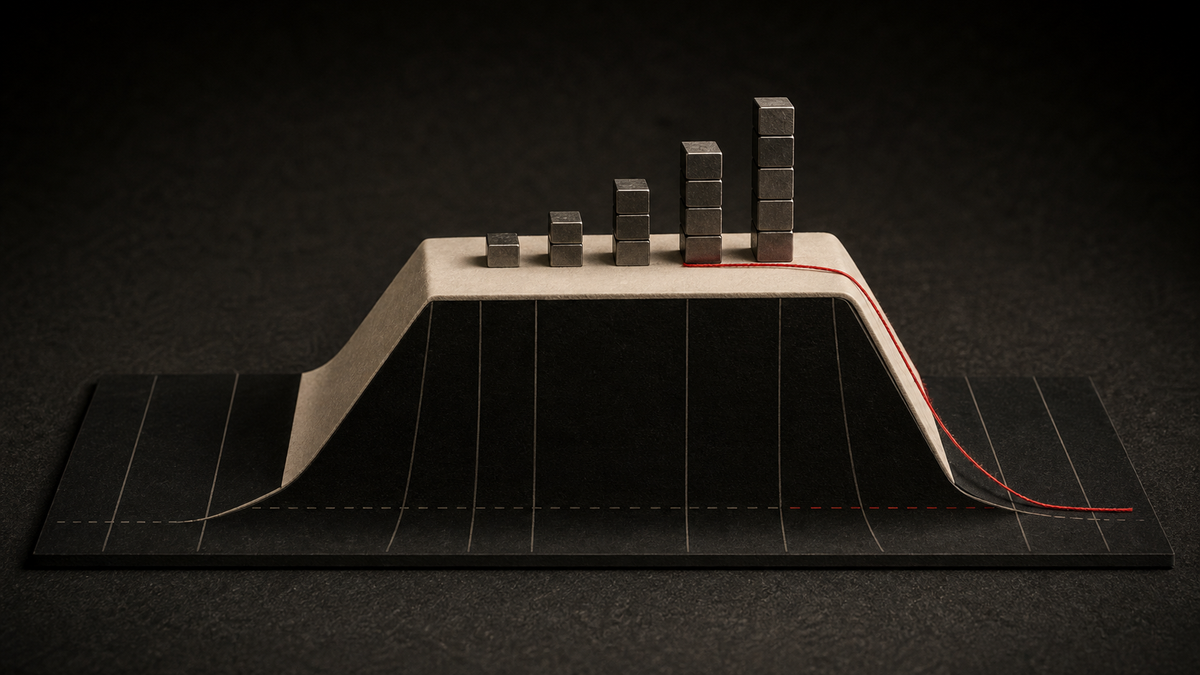

The Martingale Shape

The word that keeps following the story is "martingale."

In trading language, that usually means increasing size after losses in an attempt to win back the damage when the next trade works. The trader may not call it martingale. He may call it adjustment, rescue, rolling, conviction, recovery, or using the edge at a better price.

The account does not care what it is called.

If the next position is larger because the last position hurt, the trader has changed the problem. He is no longer only trading the market. He is trading the pressure created by the previous loss.

The pressure is harsh in short-dated options. The clock is fast. The deltas move. The trader can be right about the general idea and still wrong about the path. He can also be wrong once at a size that erases many correct smaller trades.

The basic arithmetic is not complicated:

- small premium collected many times;

- one bad move;

- larger follow-up trade;

- another bad move;

- account loss no longer proportional to the original idea.

At that point, the strategy may still have defined risk per trade. The trader does not.

The Follower Problem

The story gets worse when other people are copying the trade.

A trader can decide to put his own account through a hard options sequence. A public figure broadcasting trades to followers is a different structure entirely.

MarketWatch reported that some followers lost life-changing sums. Interactive Brokers' republished column notes that one follower had even created a GoFundMe page after the loss.

That is not just a trading detail. It is a risk-control detail.

If followers are entering later, using different fills, different account sizes, different margin treatment, different exits, and different emotional tolerance, they are not actually taking the same trade. They are taking a rough copy of a trade whose risk may already depend on precise timing and size.

This is one reason public trade-following is so dangerous in options. A stock pick can be sloppy and still be roughly similar across accounts. A short-dated options spread is not like that. A few minutes, a few points, or a different roll can change the profile.

The leader may be trading a system.

The follower may be trading a screenshot.

Defined Risk Needs A Second Number

Every defined-risk trade needs a second number.

The first number is maximum loss on the spread.

The second number is maximum loss for the sequence.

Without the second number, the trader has not really defined risk. He has defined the edge of one box and left open how many boxes he is allowed to stack.

Before entering an iron condor, the trader should know:

- maximum loss per spread;

- maximum account percentage allowed on the first trade;

- maximum account percentage allowed for the full campaign;

- whether adding after a loss is permitted;

- how many times adjustment is allowed;

- what market condition ends the idea completely;

- whether the trade is still acceptable if it hits max loss today.

The last question matters.

If maximum loss is technically acceptable but emotionally impossible, the size is wrong. If the trader needs to adjust to avoid admitting the loss, the plan is wrong. If the trade only works because the next trade can be bigger, the account is already in the strategy.

The Wrong Lesson

The wrong lesson is "never trade iron condors."

Too easy.

Iron condors are tools. So are spreads, futures, stops, leverage, and options calculators. Tools do not remove judgment. They just make certain risks easier to see and other risks easier to ignore.

The better lesson is that options traders should stop treating a payoff diagram as a risk system.

A payoff diagram shows one position at one expiration under one set of assumptions. It does not show the trader's tendency to add size after pain. It does not show follower behavior. It does not show slippage under stress. It does not show the cost of being unable to take the loss and stop.

That is where much of the damage lives.

The Desk Version

For a trader, the Captain Condor file reduces to a few checks.

Do not ask only whether the trade has defined risk. Ask whether the account has defined risk.

Do not ask only whether the range is likely to hold. Ask what happens if it breaks today.

Do not ask only whether the premium looks attractive. Ask how many ordinary wins one full loss will erase.

Do not ask only whether the adjustment lowers the pain. Ask whether it increases the size of the next mistake.

The iron condor is not the problem. The problem is the sentence that comes after the loss:

One more, larger, and I can get it back.

That sentence is enough to turn a defined-risk trade into an undefined-risk habit.

Disclosure: Margin of Pain publishes research and commentary about traders, markets, and risk. This article is not investment advice or a recommendation to buy, sell, short, or hold any security, derivative, futures contract, currency, commodity, or asset.

Source trail

- MarketWatch, "I experienced a catastrophic financial loss": How options trader "Captain Condor" led his followers to a $50 million wipeout.

- Interactive Brokers / Barron's, Are You Using Options the Right Way? Don't Fall Into This Trap.

- OptionStrat, Iron Condor options profit calculator.

- OptionStrat blog, Captain Condor's Wipeout.

- Margin of Pain, Jack Schwager and the Winning Trade That Teaches Nothing.

- Margin of Pain, The Stop Has To Be Where The Trade Is Wrong.